In the ongoing EU policy debate on post-trade market structure, there has been increasing scrutiny on the practice of internalised settlement - with some stakeholders suggesting that this may lead to diminished transparency, market fragmentation, and the potential build-up of risk outside central infrastructures.

But before reaching for new constraints, it is worth asking a simpler question: are we targeting a problem, or misunderstanding a system that already delivers efficiency, resilience and investor choice?

This is not just a technical debate about back-office processes. It goes directly to the cost of investing, the efficiency of cross-border capital flows, and ultimately the attractiveness of Europe’s markets for investors and issuers alike.

Europe’s post-trade plumbing remains poorly understood. At the centre are custodians - the quiet plumbers of Europe’s capital markets. They connect investors to issuers, keep assets safe, and make sure that trades actually settle. These functions may be invisible to most market participants, but they are fundamental to how capital moves across borders.

Crucially, the account structures and settlement practices now under scrutiny are not sources of fragility, but core enablers of efficiency. They allow a fragmented European market to function as a coherent whole. Without them, cross-border investment would be slower, more expensive and operationally complex.

This is particularly evident given Europe’s market structure. Most investors want to access multiple markets, each with its own Central Securities Depository (CSD). Direct connectivity for every investor would be prohibitively costly and operationally burdensome. Custodians solve this by aggregating demand and operating networks of sub-custodians, offering a single access point to domestic and cross-border markets in a way that remains tightly regulated under banking, securities and fund rules.

Account structures

At the CSD or top-tier level, there are two main models for holding client assets: omnibus accounts and segregated accounts. In an omnibus account, a custodian pools the securities of many underlying clients in a single account at the CSD, while maintaining detailed, client-by-client records in its own books. In a segregated account, a client’s holdings are ringfenced in a separate account at the CSD, typically in that client’s own name or otherwise clearly distinguished from other clients’ assets.

Omnibus accounts are widely used because they are flexible, scalable and cost-efficient: they simplify account opening and maintenance, streamline asset servicing, and make reconciliations more straightforward across many markets. Segregated accounts remain important where clients have specific risk, legal or disclosure preferences – the relevant regulation (Central Securities Depositories Regulation or CSDR) deliberately preserves client choice by requiring that both omnibus and segregated options are available.

In practice, both models often coexist. A global custodian might hold an omnibus account at a local CSD, but operate segregated sub-accounts for particular end-clients in its internal ledgers. Legal, fiscal and market-practice rules in some jurisdictions still constrain how flexibly these structures can be used cross-border, affecting overall efficiency of settlement routing.

Omnibus accounts and “internalisation”

These account structures directly influence how settlement is routed. When multiple clients’ positions are held in a single omnibus account at the CSD, and both sides to a trade use the same intermediary, that intermediary can settle the transaction by making offsetting updates to its own book, without updating the CSD’s records. This is “internalised settlement” under CSDR: settlement outside a securities settlement system, concluded on the books of an intermediary.

The same characteristics that make omnibus accounts attractive – pooled positions, flexibility across clients, and scalable account structures – naturally increase the scope for internalisation. If counterparties instead held only segregated accounts at different intermediaries, many more trades would need to be re-instructed to the CSD, even where there is no change needed on the CSD’s books. In other words, omnibus accounts are a key enabler of efficient internal book-entry settlement, which is generally a consequence of client and market-structure choices, not a unilateral action by custodians.

From an investor protection perspective, omnibus use does not imply weaker safeguards: intermediaries must keep precise internal records, segregate client assets from their own, and comply with strict prudential and conduct requirements1. Clients who prefer to avoid internalisation can request segregated arrangements - the fact that many do not suggests that they value the cost and efficiency gains created by omnibus structures.

The benefits of internalisation

Internalised settlement is essentially an operational optimisation: if both legs of a transaction sit on the same provider’s books, it is more efficient to move them internally rather than via a CSD. Doing so reduces external messaging, reconciliation steps, and dependence on CSDs’ processing windows , which in turn lowers operational risk and the likelihood of settlement delays or fails.

These benefits are particularly visible in use cases with high-frequency, low-risk movements, such as triparty collateral management, portfolio transitions and internal client transfers. In these settings, internalisation allows very large numbers of free-of-payment collateral adjustments or bulk reallocations to be processed quickly within a single control environment, including outside CSD operating hours, thereby tightening the link between market exposure and collateral and helping to reduce risk.

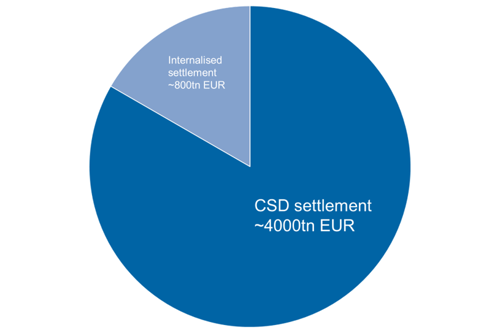

For end-investors, the impact is indirect but meaningful: smoother post-trade processing supports lower costs, better liquidity of settlement resources, and reduced friction in cross-border investment. ESMA’s own analysis has noted that internalised settlement volumes are materially smaller than CSD-processed volumes overall, and that no major risks have been identified in relation to the activity.

Figure 1: EEA settlement activity - FY2024

source: ESMA TRV Risk Monitor, No. 2 2025

Common misconceptions

However, the way internalised settlement data are sometimes presented can give a distorted impression. For example, aggregating all internalised flows without clearly distinguishing business lines (such as collateral management) or the predominance of free-of-payment movements can overstate the riskiness of the activity. Treating “settlement internalisers” as if they were a separate class of institution, rather than recognising internalisation as an activity undertaken by a wide range of regulated firms – including brokers, custodians and investor CSDs – can also be misleading.

Moreover, references that implicitly compare internalised volumes to CSD traffic, or imply that internalisation fragments “liquidity” in settlement, risk confusing trading-venue concepts (such as MiFID systematic internalisers) with post-trade mechanics. Internalised settlement neither involves balance-sheet risk-taking nor removes securities from the settlement ecosystem. It supports settlement liquidity by enabling faster, more reliable mobilisation of available inventory.

What next?

Given the current evidence, there is little to suggest that internalised settlement, or the omnibus account structures that facilitate it, warrants structural restrictions or expanded public disclosure obligations. Such measures would raise costs for investors, reduce competitive choice between providers and account types, without delivering commensurate benefits.

At a time when the EU is seeking to deepen its capital markets, these trade-offs matter. Higher friction in post-trade processes ultimately feeds through to investment costs and market attractiveness.

As ESMA continues its more granular analysis of the data, the focus should be on distinguishing between different types of internalisation activity, particularly separating collateral movements and own-account transfers.

More broadly, policy efforts would be better focused on removing legal and fiscal barriers that still limit cross-border account structures, while preserving client choice between omnibus and segregated accounts as enshrined in CSDR.

Custodians play a vital role in connecting issuers and investors in Europe’s capital markets . Regulatory policy should continue to ensure that they can do this as efficiently and competitively as possible - recognising that the “plumbers” are not the problem, but a key part of the solution.